Auditor’s Duties and Limits of Authority

In accordance with Article 41 of the Condominium Law, auditors are obliged to continuously supervise the management of the main property. In collective structures, this duty is addressed within a broader framework under Articles 69-71 of the Condominium Law; common areas, facilities, and all management activities fall within the scope of auditing. The manager must present all kinds of books, documents, and records to the auditors.

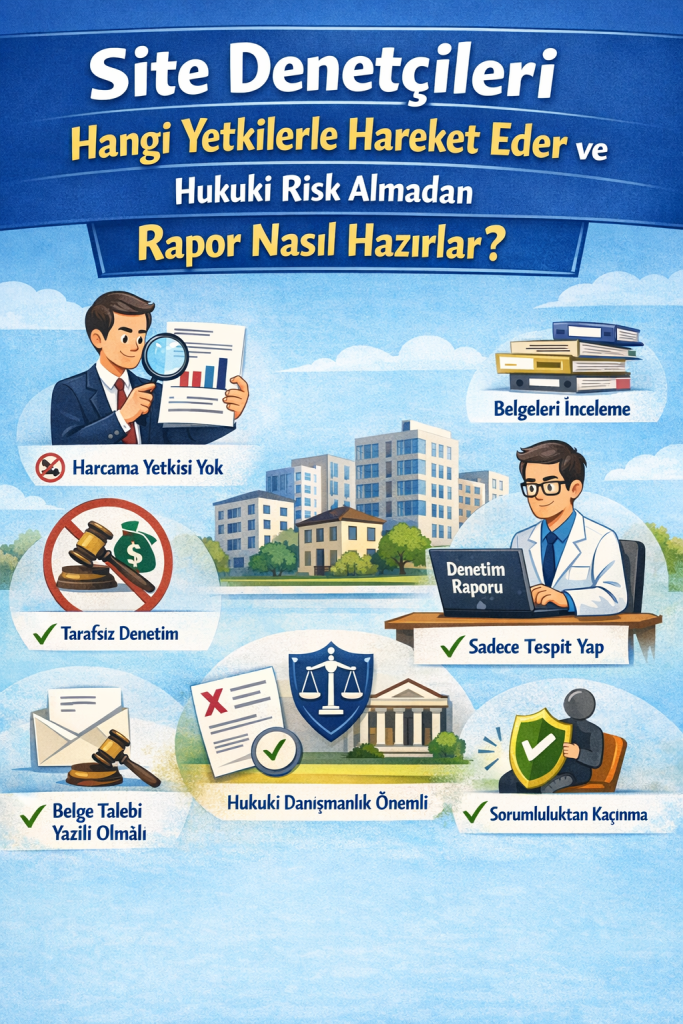

However, the critical distinction here is this: the auditor is not an “executive body” but a “supervisory body”. According to Supreme Court precedents, auditors do not have the authority to make expenditures, sign contracts, or conduct transactions on behalf of the site. Therefore, auditors cannot make decisions by replacing the management; they can only examine and report on the transactions carried out. Exceeding this limit directly places the auditor under personal liability.

Furthermore, the auditing activity must be conducted independently and impartially. The auditor must make an objective assessment without being in a conflict of interest with the management or any of the condominium owners. This obligation is a fundamental principle for the reliability of the audit.

How Should the Audit Report Be Written?

Audit reports are one of the most important documents that reveal the financial and administrative status of the site. Therefore, the most fundamental principle in preparing reports is to only make “findings”. The auditor should present the results obtained from their examinations with concrete data, but should not ascribe legal qualifications to these results.

For example; “No document could be found regarding the receipt of the service related to the invoice dated X” is a correct audit approach. In contrast, an expression like “the management has committed embezzlement” exceeds the auditor’s authority and creates legal liability. Legal evaluation and the decision for sanctions are solely within the authority of the general assembly of condominium owners.

Furthermore, in report writing, statements from parties must be clearly separated, and every finding must be based on documentation, and commentary must be avoided. The auditor should act like an expert witness; and refrain from subjective evaluations. At the same time, it is important for the report to reveal not only past transactions but also current risks, for the general assembly to make sound decisions.

What Should Be Done If the Management Does Not Provide Documents?

One of the most common problems encountered in practice is the management’s failure to provide the necessary information and documents to the auditors. However, according to the Condominium Law, the manager is obliged to present all kinds of documents to the auditors.

If this obligation is not fulfilled, auditors must make a written request. Making these requests through a notary public or via registered mail with return receipt is important for proving the process. If the management fails to provide documents, this fact must be clearly stated in the audit report.

For example; a statement like “Despite our written request dated X, the relevant documents were not submitted, so an audit could not be performed on this matter” should be used. This approach shows that the auditor has fulfilled their duty and that the deficiency originates from the management. Thus, the auditor is protected from legal liabilities that may arise in the future.

Legal Consultancy and Budget Issue

One of the issues auditors most frequently hesitate about is whether they can obtain external legal or financial consultancy. According to Article 20 of the Condominium Law, expenditures to be made within the scope of common expenses must be included in the operating plan or approved by the board of apartment owners.

Therefore, if auditors enter into a contract with a lawyer or financial advisor on their own initiative, this contract does not bind the site. The expenditure made remains directly under the personal responsibility of the auditors. The Supreme Court’s practices are also in this direction.

Furthermore, the essential elements of the audit activity (book examination, invoice control, etc.) must be carried out personally by the auditors. Expert support can only be utilized in cases requiring special and technical expertise, with the necessary budget approval. Therefore, if professional support is needed, it must definitely be put on the general assembly agenda and decided upon.

Auditors’ Legal Liability and Risks

Auditors are subject to a responsibility similar to the provisions of agency in the Code of Obligations when performing their duties. In this context, if the auditor fails to show due diligence, or prepares an incomplete or erroneous report, liability for compensation may arise.

Especially, failure to notice clear irregularities, overlooking fake or undocumented transactions, or providing a positive report without conducting an audit is considered auditor’s negligence. Supreme Court decisions also clearly state that liability will arise if auditors fail to perform their audit duty properly.

Furthermore, auditors exceeding their authority by carrying out transactions on behalf of the site is another risk area. In this situation, the auditor becomes an unauthorized representative and is personally responsible for the transactions they perform. In cases where audit reports are incomplete or erroneous, auditors may not be acquitted and lawsuits may be filed against them.

Conflict Between Legislation and Practice

One of the most significant problems observed in practice is the inconsistency between legislation and practice. The Condominium Law imposes a broad auditing duty on auditors; although it limits the necessary authority and budget possibilities for them to perform this duty.

The obligation for auditors to be chosen from among the unit owners often results in these individuals not having professional knowledge. However, in large and complex sites, there are significant financial transactions, and auditing these transactions requires expertise. This situation reduces the effectiveness of the audit activity and can pave the way for malicious practices.

Therefore, it is important for auditors in practice to work by dividing tasks, prepare reports on time, and rely on objective criteria as much as possible. Furthermore, the submission of reports for review by unit owners before the general assembly is an important practice for transparency.

Frequently Asked Questions

Denetçi site adına harcama yapabilir mi?

Hayır. Denetçilerin harcama yetkisi bulunmamaktadır. Genel kurul veya bütçe onayı olmadan yapılan harcamalar denetçinin şahsi sorumluluğundadır.

Denetim raporunda suç isnadı yapılabilir mi?

Hayır. Denetçi yalnızca tespit yapabilir. Hukuki değerlendirme ve suç duyurusu kat malikleri kurulunun yetkisindedir.

Yönetim belge vermezse denetçi sorumlu olur mu?

Hayır. Denetçi yazılı talepte bulunup belge verilmediğini rapora açıkça yazarsa sorumluluktan kurtulur.

Why is Expert Legal Support Necessary?

Site management and audit processes are complex legal areas involving high financial values and the common interests of numerous individuals. Personal liability may arise if auditors exceed their authority, prepare erroneous reports, or conduct incomplete examinations. Therefore, carrying out the process with professional support is of great importance.

Support from an expert site management lawyer or condominium law lawyer; ensures that audit reports are prepared in accordance with the law, risks are accurately identified, and potential disputes are managed effectively. Especially in large cities, Istanbul site consultancy services have become a critical need for the healthy functioning of site managements. In the Tuzla region, Tuzla site management lawyer support provides significant advantages in resolving local practical issues and differences in application.

At this point, 2M Hukuk Law Office, with its experience in site management and condominium law, provides comprehensive consultancy services that protect the rights of auditors and unit owners.