Introduction

This study analyzes the mandatory provisions that payment plans submitted to creditors within the scope of concordat projects must contain, in light of the provisions of the Enforcement and Bankruptcy Law (EBL) and current judicial decisions. The analysis reveals how courts evaluate fundamental elements such as discounts, maturities, installment payments, and payment periods offered to unsecured creditors. The study examines the practical implications of the mandatory elements stipulated in Article 305 of the EBL for the confirmation of a concordat, such as the proposal being more advantageous than bankruptcy, proportionality with the debtor’s resources, equality among creditors, and the acceptance of the project by a qualified majority.

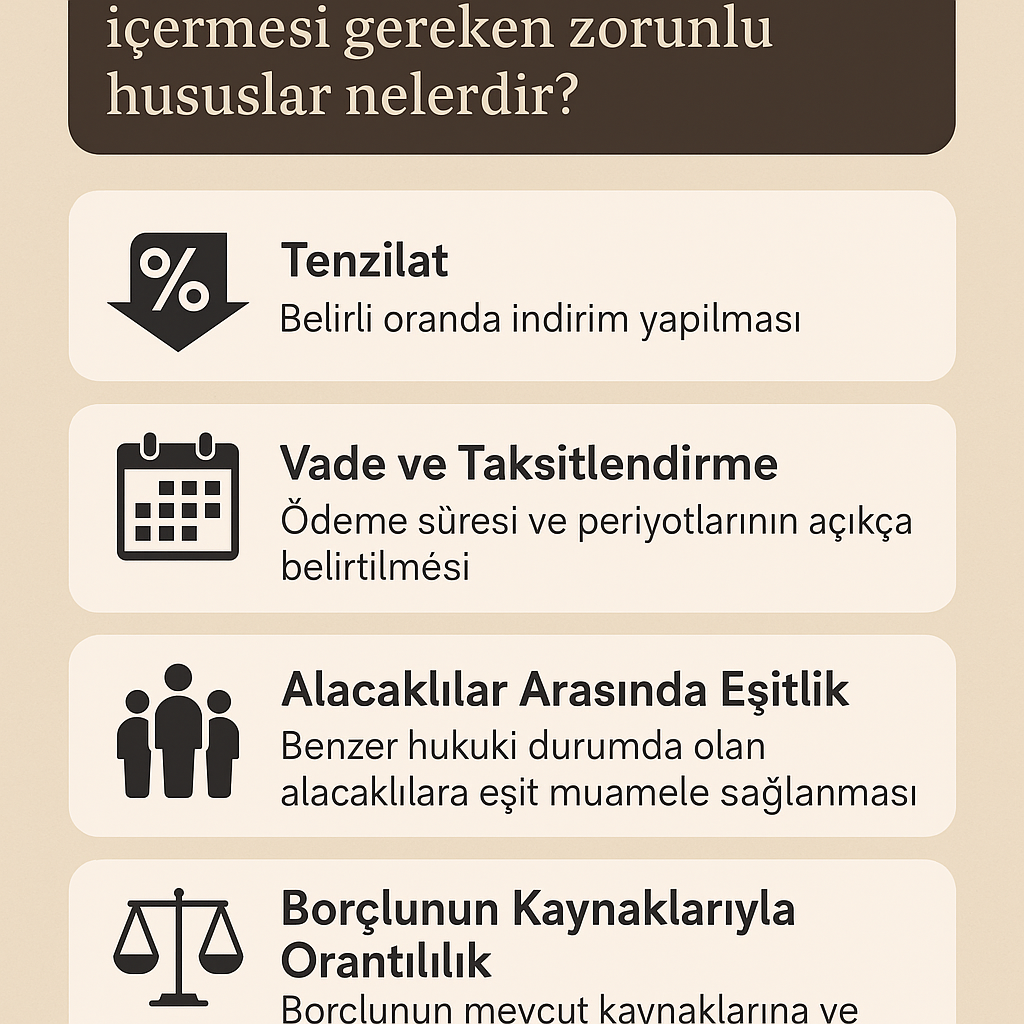

Diversity of Plans: Court decisions reveal various payment plan structures, including “concordat of reduction”, “concordat of maturity”, and “hybrid concordat”, which is a combination of the two. The plans exhibit a wide range of variations, such as discount rates ranging from 0% to 50%, interest additions, interest waivers, maturities extending from a few months to ten years, and different payment periods (monthly, quarterly, semi-annually).

Basic Confirmation Conditions (EBL Art. 305): Courts invariably seek the following cumulative conditions when confirming a payment plan:

Being Advantageous Compared to Bankruptcy: The offered amount must exceed the probable amount that creditors would receive in case of the debtor’s bankruptcy.

Proportionality with Resources: The plan must be compatible with the debtor’s current and future cash flow projections, meaning it must be feasible.

Equality Among Creditors: The plan must ensure fair, balanced, and equal treatment for all creditors in similar legal positions.

Court’s Ex Officio Correction Authority: Courts have the ex officio authority to correct a payment plan, even if it has been accepted by creditors, in accordance with Article 305/last paragraph of the EBL. Especially in situations such as the length of the term, the inequity of the grace period, or the “hidden discount” that arises against the creditor in an inflationary environment, courts intervene in the plan by shortening the term, accelerating the payment period, or moving the payment start date forward.

Reasons for Rejection and Annulment: The most common reasons for the rejection of plans or their annulment at the appellate/cassation stage are; violation of the principle of equality among creditors, the offer being disproportionate to the debtor’s resources, the use of concordat as a “cheap credit tool” with excessively long terms, and serious doubts about the feasibility of the project.

1. Discount Rate and Interest Practices in the Concordat Project

Judicial decisions reveal that the discount rate shows flexibility according to the debtor’s financial situation. While some decisions accept clear discount rates such as 20% (Bakırköy 1st ATM – 2020/447), 30% (Ankara West ATM – 2019/785), or 50% (Bakırköy 1st ATM – 2022/215), many projects commit to paying the entire principal with a 0% discount.

However, interest-free and long-term payment plans are considered by the courts as “implicit discounts”. The Antalya Regional Court of Justice, stating this situation as “an implicit discount equal to the interest rate applied to debts on an annual basis”, ruled that a company not in insolvency applying for this method is contrary to the principle of proportionality with its resources (Antalya BAM – 2024/345). Similarly, the Court of Cassation criticized the low interest rates offered in a high inflation environment as being detrimental to the balance of interests: “considering the inflation rate in our country, applying a 1% monthly interest rate despite high inflation, to the detriment of creditors, and agreeing on payment over a long period of 4 years with one installment each year” (Court of Cassation 6th Civil Chamber – 2025/2139).

In contrast, some courts have established a balance in favor of the creditor by approving plans that foresee the payment of interest in addition to 100% of the principal. For example, in one decision, the proposal of “100% of the debts subject to concordat, plus 20% interest, to be paid” was accepted, deeming it proportional to the debtor’s resources (Bakırköy 1st Commercial Court – 2024/366).

2. Maturity, Grace Period, and Installment Structure

Payment plan maturities vary significantly depending on the nature of the project. A wide range is available, from short terms of 15 months (Bakırköy 1st Commercial Court – 2024/366) to long terms of 10 years (Istanbul Regional Court of Justice 45th Civil Chamber – 2021/560). However, courts tend to view particularly long terms as detrimental to creditors. The Ankara Regional Court of Justice rejected a 60-month interest-free payment plan on the grounds that: “According to the established practice of the Supreme Court, such a long payment period is contrary to the purpose of concordat and is likely to harm creditors.” (Ankara Regional Court of Justice 23rd Civil Chamber – 2024/1607).

Grace periods are also a frequently encountered element. Grace periods of up to 6 months, 1 year, or 24 months can be offered. However, courts emphasize that these periods should not disrupt the balance of interests between creditor and debtor. The Bursa Regional Court of Justice rejected a plan with a 6-month grace period and 48 months interest-free, stating that it “disrupts the balance of interests between creditors and debtor in favor of the debtor” (Bursa Regional Court of Justice 5th Civil Chamber – 2024/1358).

Installment structures are generally arranged as equal monthly, quarterly, or semi-annual periods. However, gradually increasing payment plans aligned with the company’s cash flow (for example, 10% in the first year, 20% in the second year, 30% in the third year, 40% in the fourth year) are also accepted (Bursa 1st Commercial Court – 2022/153).

3. Principle of Equality Among Creditors

The principle of equality is the most critical mandatory element of payment plans. As stated by the General Assembly of Civil Chambers of the Court of Cassation,“the establishment of a fair and balanced payment plan that encompasses all creditors in a similar situation without making any distinction among creditors in a concordat”is essential (YHGK – 2023/620).

The violation of this principle is, by itself, a sufficient reason for the rejection of the plan. Especially, offering early or full payment to small creditors while extending payment over a long term for large creditors is considered by courts “contrary to the principle of equality” and “aimed at influencing the acceptance ratio” as a maneuver. The Court of Cassation has expressed this situation as follows: “In the concrete case, it is observed that the approved concordat project envisages a payment plan that creates a distinction between creditors with low claims and those with high claims from the plaintiff company, and that the principle of equality has been violated.” (Yargıtay 6. HD – 2022/1994).

Similarly, offering more advantageous payment terms to some creditors by entering into special protocols with them is also considered a clear violation of the principle of equality and can lead to the conclusion that the project is in bad faith (Ankara BAM 23. HD – 2023/309).

4. Proportionality with Resources and Feasibility

For a payment plan to be approved, it is essential that it is compatible with the debtor’s financial statements, cash flow projections, and operational potential. Courts make this assessment based on reports from commissioners and expert witnesses. Findings in the reports, such as “that the condition that the proposed amount will be proportionate to the debtor’s resources will have been met” (Bakırköy 1st Commercial Court – 2024/366) or “the payment plan in the project has been prepared in accordance with the plaintiff company’s operational potential and cash flow forecast” (Bursa 1st Commercial Court – 2022/153), confirm the feasibility of the plan.

Conversely, situations such as the company being insolvent, its financial statements being contradictory, or the failure to achieve targeted profits, indicate that the plan is disproportionate to the resources and lead to the rejection of the request (Istanbul Anatolian 1st Commercial Court – 2021/918; Ankara West Commercial Court – 2019/785).

Conclusion

For a concordat payment plan presented to creditors to be approved, it is mandatory to fully meet the cumulative conditions specified in Article 305 of the Enforcement and Bankruptcy Law (EBL). Court decisions indicate that great importance is attached to the principles of “equality among creditors” and “proportionality with resources” among these conditions. A payment plan gains legal validity not only by being accepted by the majority of creditors but also by being fair, balanced, consistent with economic realities, and feasible. Courts actively protect the balance of interests by using their ex officio power to correct or reject plans that deviate from the purpose of the concordat institution, providing an unfair advantage to the debtor or causing excessive damage to creditors. Therefore, meticulously observing all these mandatory considerations when preparing a payment plan is of vital importance for the project’s success. An article suggestion.

Why is expert concordat lawyer support necessary?

This study examines the mandatory elements that payment plans presented to creditors within the scope of concordat projects must contain, in light of the provisions of the Enforcement and Bankruptcy Law (EBL) and current court decisions. It is observed that courts, when evaluating concordat plans, strictly adhere to criteria such as discount rate, maturity, interest, the principle of equality, proportionality with resources, and the feasibility of the plan. In practice, many concordat requests are rejected due to the lack of just one of these elements, or even if approved, they are overturned by higher courts.

Court decisions clearly show that, the success of a concordat plan requires technical and strategic legal knowledge. Every concordat plan is not only a debt payment schedule but also a project that legally grounds the debtor’s will to sustain their economic existence. A small calculation error, missing document, or a regulation contrary to the principle of equality made during this process can lead to the complete rejection of the concordat request. For this reason, a concordat plan to be prepared in a way that protects the interests of both debtors and creditors, has become a necessity to be created under the supervision of expert concordat lawyers.

2M Law Firm provides professional consultancy at every stage of the concordat process to businesses operating in the Istanbul, Tuzla, Pendik, Maltepe, Umraniye, Kartal, Maltepe, Gebze, and Tepeören regions. Our experienced concordat lawyers offer comprehensive legal support for the preparation of payment plans in accordance with legal requirements, the creation of an acceptable structure under the supervision of the court and commissioner, and the successful completion of the ratification process. A properly structured payment plan is not just a step towards debt relief, but also a fundamental step in the restructuring of the business — therefore, expert lawyer support is vital at every stage of the concordat process.